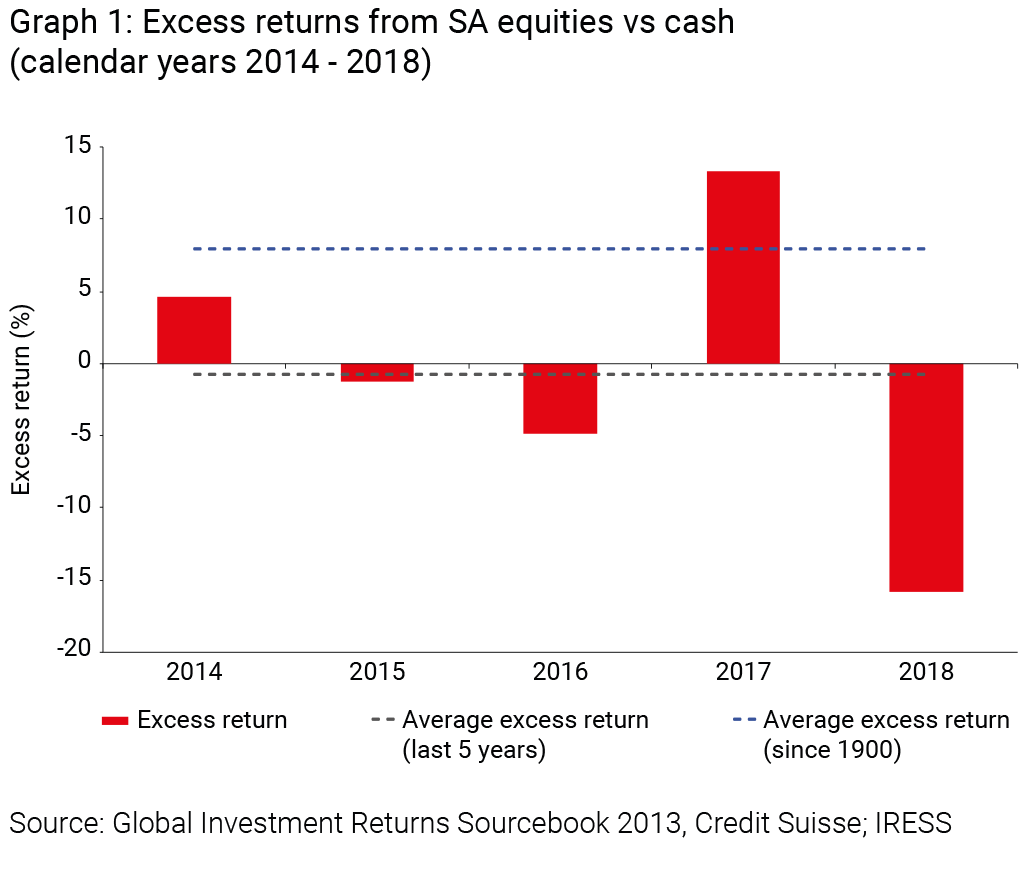

Graph 1 puts the last five calendar years into perspective. It assumes that each year an investor had a choice to invest in the FTSE/JSE All Share Index (ALSI) or in cash and calculates the excess return the investor received: When the red bar is above zero, equities performed better than cash, and vice versa. One can immediately see what a tough period it has been for equity investors despite Naspers returning a cumulative 167% over the period. Indeed, the simple five-year average excess return is now negative in contrast to the 118-year average of 8%.

We’ve been here before

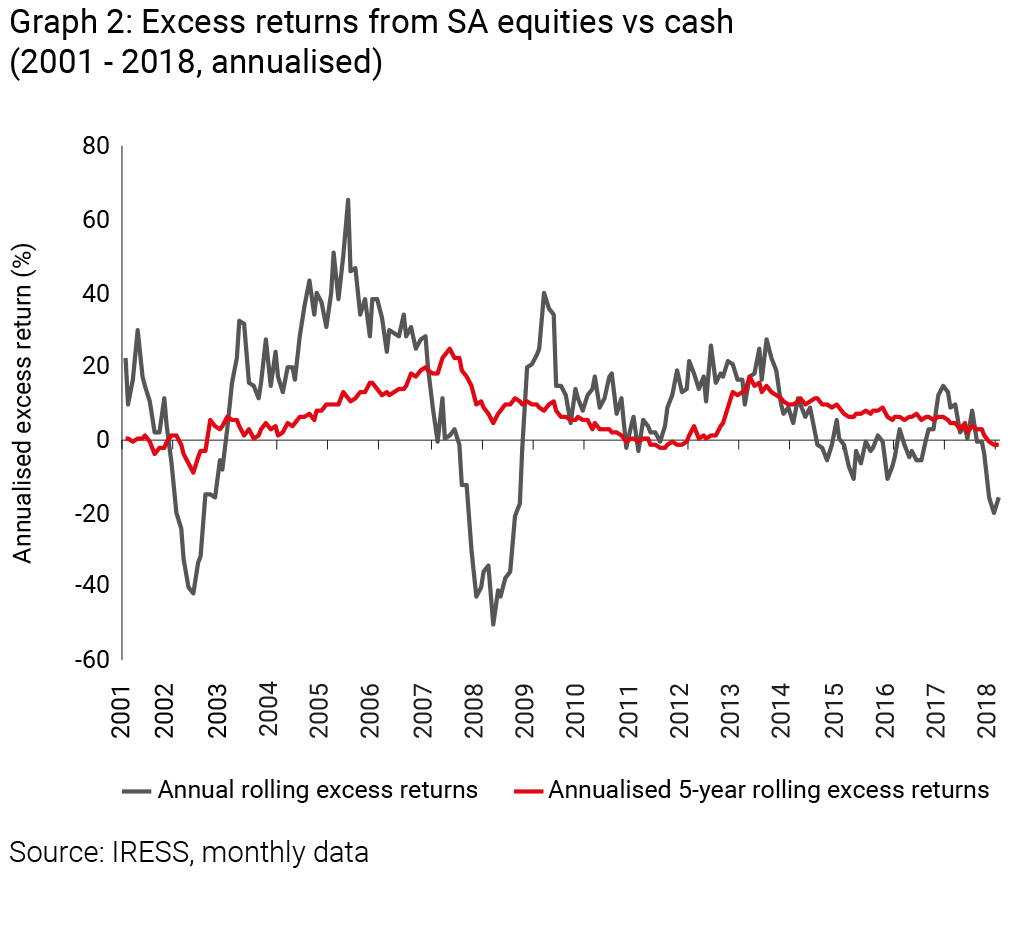

This period feels somewhat similar to 2002 and 2003 when South African equities had underperformed cash over the prior five years, as shown by the red line in Graph 2. The annual excess returns shown by the grey line were particularly poor, with equity investors experiencing significant underperformance during 2002 and 2003. With valuations low and sentiment negative, the market was priced to (and did) embark on a great bull run (even when measured in US dollars) following that period of poor performance from equities. We must however state that today’s valuations are not as low as they were then.

What about the really long-term picture?

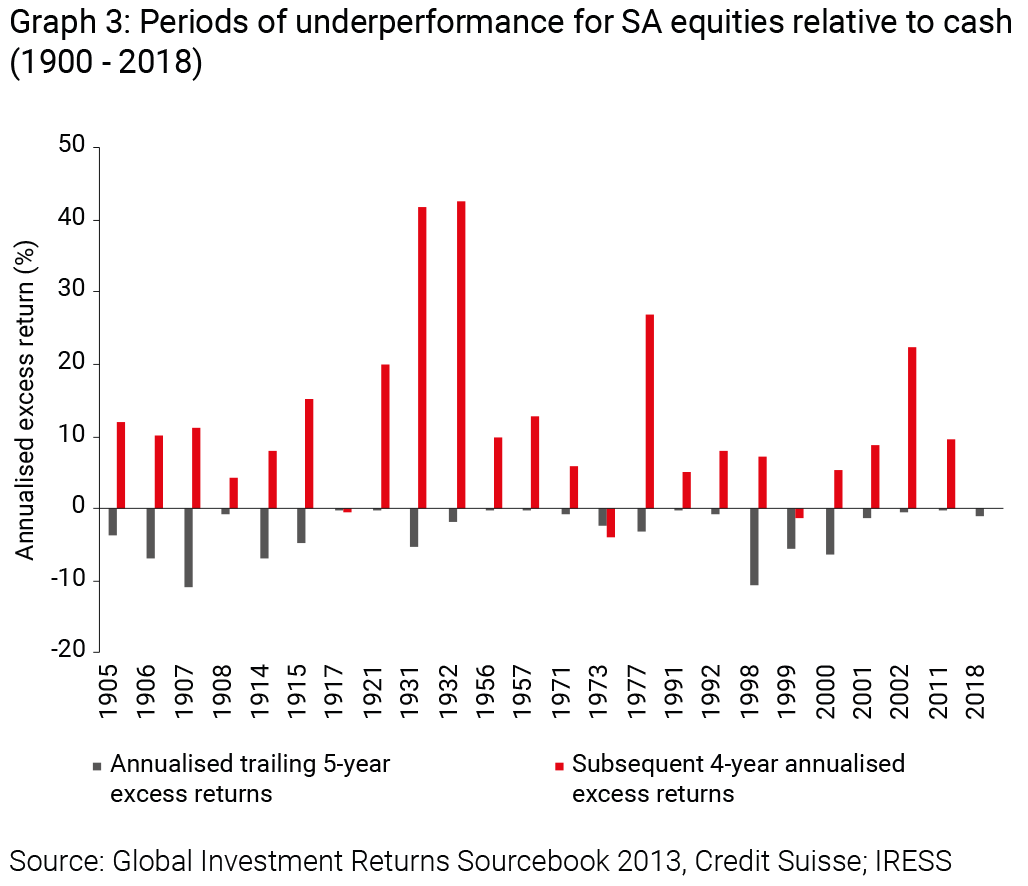

Graph 3 highlights periods when South African equities had underperformed cash over a five-year calendar period starting in 1900. These periods are represented by the grey bars.

The red bars represent the subsequent four-year excess return of equities versus cash (we normally assess potential investments on a four-year view). Besides the point that you did not want to be significantly overweight equities going into the Great Depression (1929) and the Asian financial crisis (1997), the data does show a generally pleasing picture of strong outperformance by equities after the periods of underperformance. After such points in time, as shown in the grey bars, where equities have underperformed cash, the subsequent four-year excess returns have been positive over 85% of the time, with the average annualised four-year excess returns more than 50% higher than their long-term average.

Light at the end of the tunnel?

It takes depressed valuations and negative sentiment to set the ground for strong excess returns. With the ALSI, when measured in US dollars, at the same level it was in April 2007, it should be no surprise that we are finding more opportunities in South African equities than we have for some time (other than the brief few months during what has become known as Nenegate).

While one cannot be sure what lies ahead, history strongly suggests that there is a higher probability of a positive rather than a negative outcome for equity investors who have a long-term investment horizon. The ALSI has been valued lower before and companies’ profits are under pressure, but now does not appear to be the time to have 100% of your assets invested in rand-based money market funds.

Source: https://www.allangray.co.za/